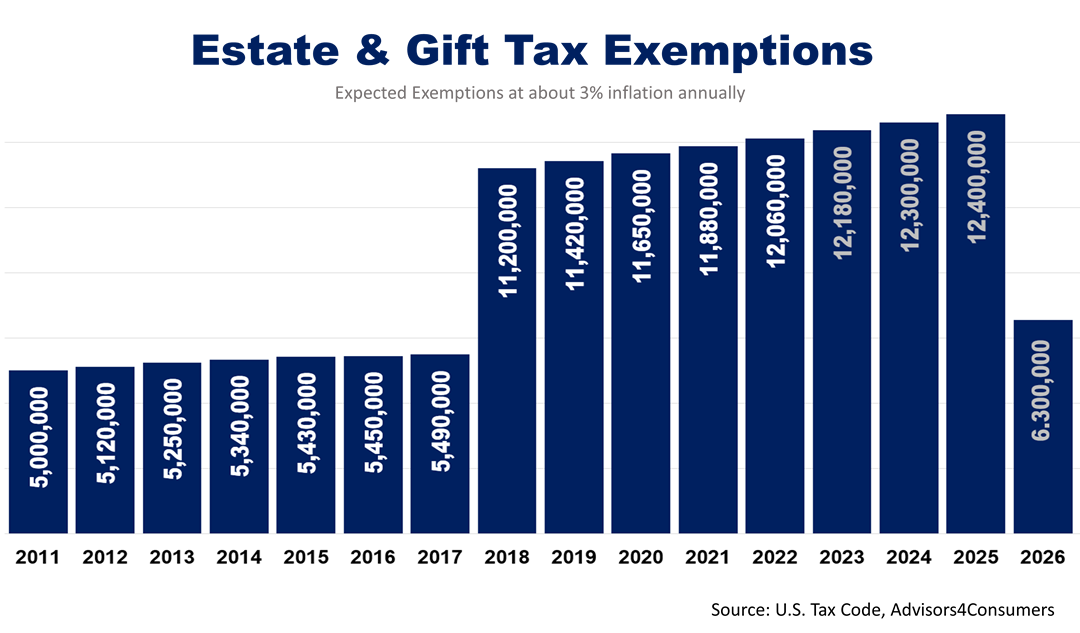

In 2022, the lifetime exemption from gift and estate tax is $12.06 million. Under current law, which is unlikely to be changed in Congress, the exemption rises annually through 2025 based on the inflation rate. With inflation in the first half of 2022 soaring at an annual rate of 8.6%, the exemption from estate and gift taxes will be about $12,180,000 in 2023. After 2022, inflation is expected to revert to its historical norm of 3%, so an estimated $12.4 million of your estate will be tax exempt in 2025. Thus, a married couple is expected to be able to pass nearly $25 million to their heirs from estate and gift tax. At that point, the estate tax will affect a fraction of American taxpayers; it’s as if it were repealed. Then, boom! In January 2026, the exemption from estate and gift tax estate tax is scheduled to be slashed in half to $6.3 million! Suddenly, the estate tax will take a bite out of the wealth of many more households. Doctors, lawyers, business owners, and their heirs are likely to see estate tax diminish their wealth, wealth that took a lifetime to build. With real estate, stocks, and other capital-gain investments appreciating sharply in recent years, individuals with large estates should be thinking now about how to take full advantage of the current exemption rules. If you want to reduce taxes on the wealth you leave to your family and protect assets from liability and creditor risk for decades to come, plan it out now -- while you have this chance. Your grandchild may be a toddler today, but you can shield them from losing family assets in a divorce 30 years from now. Likewise, you can shield your children’s assets from professional liability or business creditors. Years after you’re gone, say your grandchild becomes a doctor or landlord, planning now can eliminate the risk of property you leave being subject to a lien against your heirs’ creditors. Planning now can ensure you keep a vacation home, time share, and other assets are kept out of reach of your heirs’ creditors. Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances.

The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |