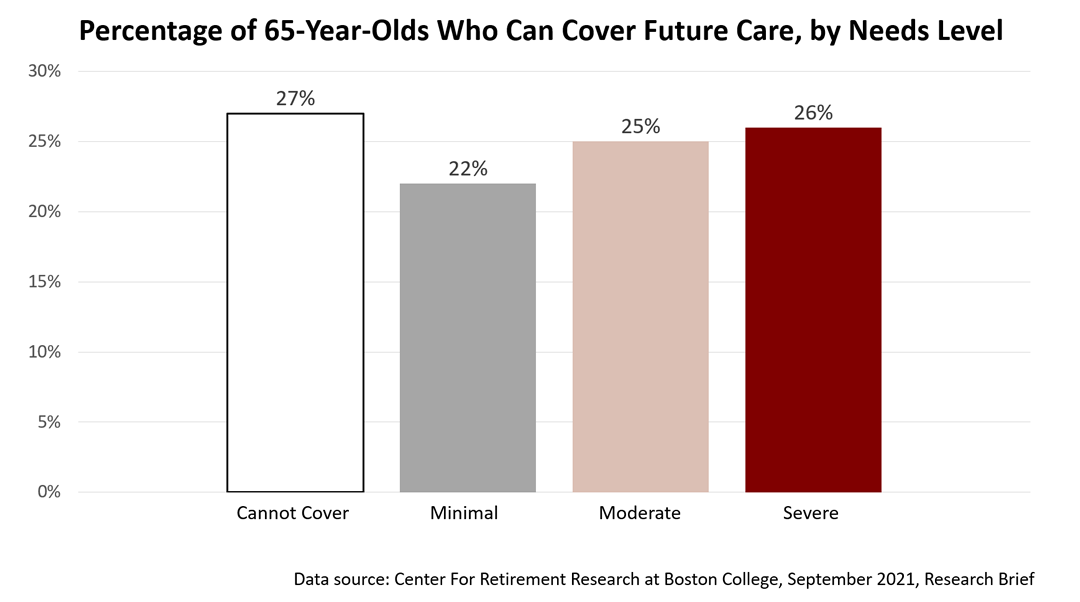

At age 65, only about 20% of American retirees have family and financial resources to cover high-intensity care for at least three years. About 30% cannot afford any help at all. The remaining half of older adults lie somewhere in between, depending on their marital status, education, and race. These are the grim conclusions of The Center for Retirement Research (CRR) at Boston College. CRR is part of a consortium of research groups funded by the U.S. Social Security Administration since 2018 and its authoritative research has painted a gloomy picture of the retirement struggle most Americans are facing.

In a September 2021 research brief, CRC examined the resources 65-year-olds have available to meet their needs for different long-term services and supports (LTSS). CRC’s analysis considered “informal” care from family members, as well as care paid for out of a retiree’s pocket, and it categorized older adults by their ability to afford minimal, moderate, and severe care needs. With about a third of America’s retirees not having the resources for even minimal care and only a fifth able to afford severe care, as baby boomers age this retirement crisis is expected to cause enormous social and political issues in the decades ahead. However, even if you have family support and enough money to care for a severe health event requiring long-term care, proper planning requires answering some difficult personal financial questions: - Can you afford to self-insure in your old age?

- Have you done the financial math to ensure you could pay for a severe-care event in your retirement years, figuring on living through age 85 or 90?

- Have you paid for long-term care insurance that has grown more expensive or provides lower benefits than it used to?

The earlier you get started on planning your retirement portfolio and income needs, the easier it is to find solutions and gain peace of mind.Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances. The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |